IREDA 8.80% Tax-Free Bonds – February 2014 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

The last leg of the current financial year’s tax-free bond issues is all set to begin early next week with IREDA and Ennore Port issues. While IREDA is next in line to issue its tax-free bonds from Monday i.e. 17th of February, Ennore Port issue is also scheduled to open the very next day i.e. Tuesday.

Though the IREDA issue is scheduled to officially close on March 10th, the company has the right to either preclose the issue or extend it depending on the investors’ response.

Before we check out other regular features of the IREDA issue, let us first try to know more about the company and its financials, as only a very few people have heard about this company in the past.

Profile of IREDA

Indian Renewable Energy Development Agency Limited (IREDA) is a wholly-owned government of India (GoI) enterprise and operates under the administrative control of the Ministry of New & Renewable Energy (MNRE). IREDA finances renewable energy & energy efficiency projects and operates a revolving fund for promotion, development and commercialization of new and renewable sources of energy.

The sectors financed by IREDA can be broadly classified under – wind energy, hydro energy, bio energy, solar energy, energy efficiency and conservation, and emerging technologies.

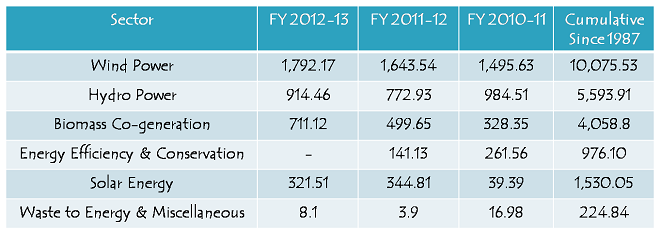

Loans Sanctioned by IREDA (Rs. in crores)

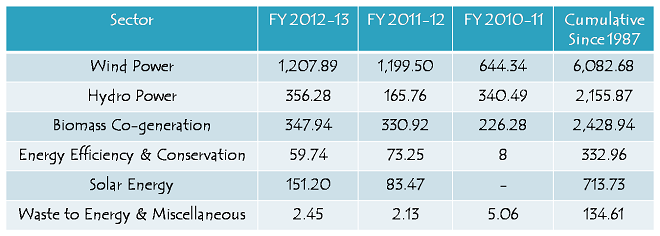

Loans Disbursed by IREDA (Rs. in crores)

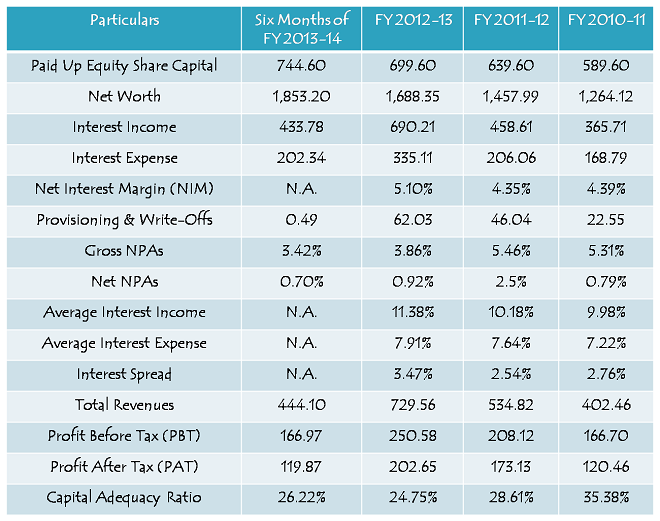

Financials of IREDA

During the financial year ended March 31, 2013, IREDA reported profit after tax (PAT) of Rs. 202.65 crore on total revenues of Rs. 729.56 crore as against PAT of Rs. 173.13 crore and revenues of Rs. 534.82 crore during the financial year ended March 31, 2012. Its relative performance during six months ended September 30, 2013 seems reasonably satisfactory with a PAT of Rs. 119.87 crore and revenues of Rs. 444.10 crore.

The company has also been able to improve on its interest rate spread and non-performing assets (NPAs) in the past one year or so.

Now, let us quickly check out the main features of this issue:

Size of the Issue – While IREDA has set the base size of the issue at Rs. 500 crore, the total issue size stands at Rs. 1,000 crore, including the green shoe option of Rs. 500 crore.

Rating of the Issue – Credit rating agencies CARE and Brickwork Ratings (BWR) have assigned ‘AAA’ rating to the issue, which is again the highest rating by any of these rating agencies, indicating lowest credit risk and thus highest safety for the investors’ investments.

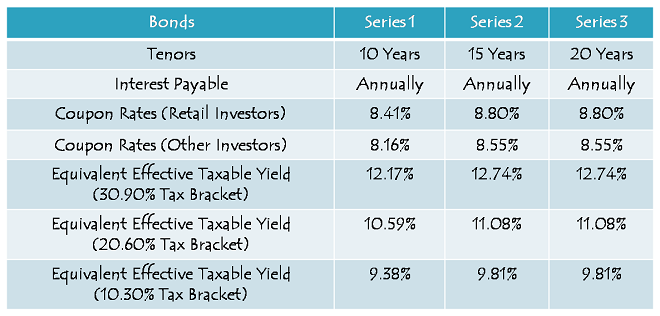

Interest Rates on Offer – Due to a jump in the 15-year and 20-year G-Sec yields after the RBI hiked Repo Rate in its monetary policy last month, IREDA issue carries higher rates for these respective tenors at 8.80% per annum. At 8.80%, IREDA’s 15-year option interest rate stands higher than 8.75% NHAI issue was offering and 8.65% IRFC issue carried for 15 years.

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and as always each category will have certain percentage of the issue reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 100 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue i.e. Rs. 200 crore is reserved

Category III – High Net Worth Individuals including HUFs – 30% of the issue i.e. Rs. 300 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 400 crore is reserved

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing, Lock-in Period, Premature Redemption – The company has decided to get its bonds listed on the Bombay Stock Exchange (BSE) as well as on the National Stock Exchange (NSE). Like with the past issues, these bonds will also get allotted and listed within 12 working days from the closing date of the issue.

There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they will get listed for trading.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will get credited to your linked bank account through ECS.

Interest on Application Money & Refund – IREDA will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – The company has decided to keep the face value of these bonds as Rs. 1,000 and the investors will be required to apply for at least five bonds to participate in the offer.

Interest Payment Date – Like many issues in the past, IREDA has not fixed its interest payment date as yet and the first due interest will be paid exactly after one year from the deemed date of allotment.

As far as the safety of the investors’ investments is concerned, I would like to mention it here that MNRE (GoI) has issued a “Letter of Comfort” to IREDA which states, inter alia, that the Ministry has been infusing equity capital into the company to support its business plans and will continue to support it in future as well whenever required. Besides, the Ministry will ensure that IREDA meets its payment obligations on these tax free bonds in a timely manner.

The issue looks reasonably good to me from the long-term investment point of view. The only thing which is required to earn capital gains from these tax-free bonds is a healthy fall in the G-Sec yields.

Application Form of IREDA Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IREDA tax-free bonds, you can contact me at +919811797407

I have some money, should I invest in tax free bond or with ppf ?

I do not have any tax exemption though

I think if you don’t require tax exemption with your investment and if you have a demat account, then tax-free bonds make more sense. If you don’t require liquidity in the long-term and are not willing to take any risk with your investment, then I think PPF is a better option.

Hi Shiv,

1. As the interest rate is same for 15 yrs & 20 yrs category. Which option to go for? 15 Yrs or 20 Yrs? Where the maximum volume will get traded?

2. What are chances that this bond will get oversubscribed on Day 1 itself?

Thanks!!

Hi Sanjay,

1. I am not sure which tenure will have the maximum demand from the institutional/corporate investors, but personally I would opt for the 20-year option. I think the retail investors would go for the 15-year option.

2. I am not sure about this also. I think it should get oversubscribed either on the first day itself or maximum second day.

Wondering if the Ennore Ports interest rates and issue details be known before the IREDA opens on 17th Feb?

Isn’t Ennore port coming out with 9% ?

which one is better Ennore (AA) at 9% or IREDA (AAA) at 8.8 ?

Which is better depends on goals . AAA is better than AA in any comparison. if you would like to trade the bonds at a later date , IREDA makes more sense with AAA rating. If you are looking to hold for entire tenure and earn .12% more return , then Ennore port is better. I would go for IREDA as it is AAA rated and .12% higher return on AA rated bond is not worth the risk

Regards

Ramadas

Hi Ramadas,

How come 0.12% extra? I think it is 0.20% extra, am I missing something?

Hi Shiv

You are right. My mind was stuck at 8.88%. I see the rates are 8.8%. Still i prefer IREDA 🙂

Regards

Ramadas

🙂 Sure, thanks for your views !!

To me both are equally good, with a slight bias towards the IREDA issue.

Ennore Port rates are already out. As Ennore Port issue is ‘AA’ rated, its rates are 20 basis points (or 0.20% p.a.) higher than the rates IREDA is offering.

Shiv, will you be doing a ‘pro-con’ comparison between these 2 with your own views on them?

Hi KS,

I’ll be travelling from today evening till Monday morning. I’ll try to cover the Ennore Port post today itself and the comparison between the two either on Monday or Tuesday.

Missing the Like button here now … after hating it for years on FB!

‘Like’ button is there for the post above, not here for the comments though !!

Hi Shiv,

As you have mentioned NRIs are not allowed to invest in these bonds. But i came across article below, which says RBI has allowed NRIs to invest in tax free bonds. Can you please confirm if NRIs are allowed or not ?

http://articles.economictimes.indiatimes.com/2013-12-25/news/45561782_1_ashutosh-khajuria-investor-base-fixed-deposits

Hi Ketki,

NRIs are not allowed to invest in this issue for sure. I think it depends on the company whether they are authorized/willing to issue tax-free bonds to the NRIs or not.

Oh! … Just looked at that. That looks like FB’s own like button. Wonder if that post a like on my F

Oh! Ok! … That looks like the std FB’s like button. I suppose it will post my Liking for this post on FB. Btw: do you know of any way to subscribe to a post (i.e. for tracking followup comments on a Post) without first making a comment; let me know.

IIFCL issue also opening on 17-Feb with 8.80% for 15 and 20 yrs. Issue size approx 2800 Cr.

Thanks Sanjay, I’ll cover it by today evening.

Hi Shiv,

Going by the upward tendency of bond yields, and the obvious incapacity to “talk” them down (of the central bank or a desperate finance minister) and what appears to be a collective incompetence and will of the government to target inflation (or anything else that is meaningful to the common man and not just to the interests of the rich that determine this country’s policies), I wonder if TFB interest rates would come down any time soon. That being the case, would FY15 afford a possibility of more 9+% offerings? What are your thoughts on this?

Hi Rama,

My personal view is quite similar to yours, but I would blame the government policies for the mess we are in and I think future yield movement will depend on various measures the next government will take for the Indian economy. Nobody is sure whether we’ll have tax free bonds next year or not. I am optimistic that we’ll have lower G-Sec yields.

Comment from my side – RBI has categorically stated that the last Jan 14 hike is the last one and that there will be no further rate hikes in the near future. I would not expect further rate hikes unless there is a sharp northward move in inflation rates. Current CPI/WPI data statistics do not indicate such a possibility.

Let’s hope the interest rates peak out soon and we have good capital appreciation in these bonds.

today’s subscription figures pls.

IREDA 1st day subscription … I saw some surprising data out here:

http://www.bseindia.com/markets/publicIssues/EODCumlativeShedule.aspx?ID=768o

Dont know if this is the right place to see?

-KS

Which data surprised you KS?

From the BSE site data, I thought the retail was already over-subscribed 1.43 times (on 200 Crores). That surprised me. But obviously you are counting on 400 Cr including i.e. the green-shoe option, that you are calling as Reserved Amt.

Still a bit surprising to see Retail at such a high %age (285.51/400) subscribed than any of the other categories.

Good to see you back fast from your weekend vacation to clarify things for us aam aadmis. Thanks.

🙂 Thanks

I am not at all surprised by the subscription figures. Institutional investors are smart investors and the retail investors always start late due to lack of knowledge/guidance.

Sorry that link had an extra ‘o’ at end, the link should have been:

http://www.bseindia.com/markets/publicIssues/EODCumlativeShedule.aspx?ID=768

KS

Thanks a lot KS for the link!

Day 1 (February 17) subscription figures:

Category I – Rs. 10 crore as against Rs. 100 crore reserved

Category II – Rs. 50 crore as against Rs. 200 crore reserved

Category III – Rs. 63.40 crore as against Rs. 300 crore reserved

Category IV – Rs. 285.51 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 408.91 crore as against total issue size of Rs. 1,000 crore

Other subscription figures not very encouraging apart from Category 4.

With most earlier issues Retail %subscribed would trail far behind other categories! This time something has changed? The 2nd status shows Retail subscription is nearing the Reserved amount too. Same Link works:

http://www.bseindia.com/markets/publicIssues/EODCumlativeShedule.aspx?ID=768

On the other hand, IIFCL subscription shows the opposite. That shows how Institutional investors view the current options differently from retail investors.

For the retail investors, interest rates come first, then comes credit rating and then the company itself. For the non-retail investors, the company comes first, then comes credit rating and then interest rates.

Also we already applied in IIFCL in the last round so opting for IREDA this time

What are the rates offered by IIFCL tranche 3 bonds?

Hi Shashwat,

IIFCL interest rates are absolutely same as the IREDA rates.

Any word on date for IRFC-II ?

Hi Raj,

Tentative launch date for IRFC Tranche II is 24th February.

Please send me all news on my email

Todays subscription figures please.

Day 2 (February 18) subscription figures:

Category I – Rs. 10 crore as against Rs. 100 crore reserved

Category II – Rs. 59.15 crore as against Rs. 200 crore reserved

Category III – Rs. 86.13 crore as against Rs. 300 crore reserved

Category IV – Rs. 370.98 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 526.26 crore as against total issue size of Rs. 1,000 crore

Day 3 (February 19) subscription figures:

Category I – Rs. 10 crore as against Rs. 100 crore reserved

Category II – Rs. 64.57 crore as against Rs. 200 crore reserved

Category III – Rs. 89.47 crore as against Rs. 300 crore reserved

Category IV – Rs. 406.61 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 570.66 crore as against total issue size of Rs. 1,000 crore

Hi Shiv,

Thanks for the wonderful articles !!

When IRFC tax free bonds will open and what are the interest rates ?

Also which is better between IREDA and IRFC ?

Thanks Prashant for your kind words !!

Tentative opening date for the IRFC issue is February 24th and the interest rate should be similar to that of IREDA/IIFCL Tranche III. I think IRFC issue is better than IREDA.

Thanks for the prompt reply !!

You are welcome Prashant!

Hi Shiv,

Question on ‘interest paid’ on the allotment money for TFBs for the period between application date and allotment date. Are they taxable income?

How about ‘interest paid’ on money refunded / returned?

Thanks,

Ram

Both are taxable Ram!

Category 4 already crossed 400? If I invest now what are my chances of getting 100% allotment?

Category IV – Rs. 406.61 crore as against Rs. 400 crore reserved

Hi Hemant,

It depends on the subscription figures of non-retail categories when the company decides to close this issue. I would say one should not invest in this issue now and wait till the issue closing date or one day prior to that. If non-retail investors don’t subscribe to this issue, only then a retail investor should go for it.

Thanks for your advice Shiv. I’ll go for Ennore port, even though the rating is low, I am planning to hold it till maturity and think that rating does not matter much.

That’s Great!

Day 4 (February 20) subscription figures:

Category I – Rs. 10 crore as against Rs. 100 crore reserved

Category II – Rs. 68.23 crore as against Rs. 200 crore reserved

Category III – Rs. 93.12 crore as against Rs. 300 crore reserved

Category IV – Rs. 431.16 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 602.52 crore as against total issue size of Rs. 1,000 crore

Day 5 (February 21) subscription figures:

Category I – Rs. 10 crore as against Rs. 100 crore reserved

Category II – Rs. 73.18 crore as against Rs. 200 crore reserved

Category III – Rs. 98.27 crore as against Rs. 300 crore reserved

Category IV – Rs. 447.02 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 628.48 crore as against total issue size of Rs. 1,000 crore

Day 6 (February 24) subscription figures:

Category I – Rs. 10.10 crore as against Rs. 100 crore reserved

Category II – Rs. 99.33 crore as against Rs. 200 crore reserved

Category III – Rs. 107.37 crore as against Rs. 300 crore reserved

Category IV – Rs. 462.63 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 679.44 crore as against total issue size of Rs. 1,000 crore

Few more TFB issues are coming up starting next week. For a 10-year maturity bucket, a retail investor can earn a coupon of 8.44 per cent while it is 8.88 per cent and 8.86 per cent for 15 and 20 years, respectively. See link below.

http://articles.economictimes.indiatimes.com/2014-02-24/news/47635732_1_irfc-indian-railway-finance-corporation-rural-electrification-corporation

Thanks Sailesh for this info !!

http://www.thehindubusinessline.com/markets/stock-markets/irfcs-second-taxfree-bond-issue-opens-on-friday/article5726490.ece

IRFC and REC issue opening on 28th with identical interest rates

Thanks Shashwat for this info !!

Day 7 (February 25) subscription figures:

Category I – Rs. 10.10 crore as against Rs. 100 crore reserved

Category II – Rs. 101.51 crore as against Rs. 200 crore reserved

Category III – Rs. 115.30 crore as against Rs. 300 crore reserved

Category IV – Rs. 471.24 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 698.15 crore as against total issue size of Rs. 1,000 crore

Day 9 (February 28) subscription figures:

Category I – Rs. 10.10 crore as against Rs. 100 crore reserved

Category II – Rs. 107.42 crore as against Rs. 200 crore reserved

Category III – Rs. 119.16 crore as against Rs. 300 crore reserved

Category IV – Rs. 486.07 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 722.75 crore as against total issue size of Rs. 1,000 crore

hi

You invest INR 1 Lac in PPF and IREDA (catIV at 8.8% coupon rate(???)if you calculate cash flow after 15 years-

IREDA= INR 231750.00

PPF= INR 351916.00 ( at 8.75% int rate)

still people advocate IREDA????

There are plenty of benefits of PPF , at the same time plenty of disadvantages as well

1) You can only invest 1 Lakh in PPF and worst case 2 Lakh if investment in name of spouse is considered. If you have surplus more than 2 Lakh , PPF will not help

2) PPF will NOT provide any capital appreciation in case interest rate fall. Assuming interest rate falls to 7% , IREDA tax free bonds will give you return in excess of 20% for a 20 year bond.

3) PPF has no liquidity other than partial withdrawal allowed after 7 years. Tax free bonds have no such lockin and people can sell anytime. One can always argue liquidity is lower , but i have never faced any issue in selling tax free bonds as long as you are not selling small amounts

4) For people who would need regular income , say yearly as interest , PPF will not help. Tax free bonds will be a huge advantage for people looking for regular income

5) PPF interest rate can vary year after year. It can even fall to 7% or 6.5% once interest rates fall. Tax free bonds once you lock in interest rates you are locked at a higher rate. Chances of Interest rate going up from here is minimal as it is detrimental for economy. So PPF may not have interest rate advantage over a 20 year period

6) I am not sure what kind of calculation you have made to get this cash flow calculation. In my calculation , assuming PPF quota of 2 lakh is already exhausted , if you invest 2 Lakh in a tax free bond and reinvest interest payout in an equity mutual fund for 15 years , you can comfortably beat PPF payout with capital protection

Comparing IREDA tax free bonds with PPF is comparing apples to oranges. Which is better depends on specific customer and each has its own benefits and disadvantages

Regards

Ramadas

Thanks, Ramadas, for this excellent and detailed comments and comparison. I agree with all your pro-con points here! For your first 1 lac of savings always put in PPF …. for more look at other avenues per your risk profile. Esp. for Sr Citizens (like me) these TFB are lucky and timely opportunity!

Thanks Ramadas for these pros and cons comparison between PPF and TFBs !!

At present I think tax free bonds as an investment package are much superior to your PPF investment. As far as credit quality and the risk of interest rates moving up are concerned, I think PPF is better. I think these are the only two factors which make PPF superior in the current scenario.

Also, PPF investment provides tax benefit u/s. 80C which is not there with tax free bonds. That is one more plus point with PPF.

Hi Yash,

How have you calculated Rs. 2,31,750 for IREDA ?? There is no compounding interest option with any of the tax free bond issues.

interst rate comes out to be 5.8% in case of IREDA compounded annually!!! for above calculated cash inflow

Yash, interest on TFB is paid annually which can be reinvested unlike PPF where the entire amount is paid on completion of 15 years. If annual interest of Rs. 8800, on investment of Rs one lakh, is reinvested at 8.8%, net amount payable would be marginally higher for TFB.

I completely agree with you Gurdeep.

IREDA has decided to close its tax free bonds issue tomorrow i.e. March 4th.

Day 10 (March 3) subscription figures:

Category I – Rs. 10.10 crore as against Rs. 100 crore reserved

Category II – Rs. 107.45 crore as against Rs. 200 crore reserved

Category III – Rs. 120.21 crore as against Rs. 300 crore reserved

Category IV – Rs. 490.84 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 728.61 crore as against total issue size of Rs. 1,000 crore

The issue closes tomorrow.

Day 11 (March 4) subscription figures:

Category I – Rs. 10.10 crore as against Rs. 100 crore reserved

Category II – Rs. 107.80 crore as against Rs. 200 crore reserved

Category III – Rs. 121.55 crore as against Rs. 300 crore reserved

Category IV – Rs. 496.60 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 736.05 crore as against total issue size of Rs. 1,000 crore

The issue stands closed today.

‘AAA’ rated NHB tax free bonds issue is getting opened on March 7th with the following coupon rates – 8.50% p.a. for 10 years, 8.93% p.a. for 15 years and 8.90% p.a. for 20 years. Issue size is Rs. 1,000 crore and will get closed on March 18th. NRIs cannot apply in this issue.

Hey Shiv,

When can we expect the allotment from IREDA ?

Thanks,

Gaurav

Hi Gaurav,

It should happen on or around 14th/18th of March.

I got my allotment of the bonds yesterday in my demat account. Should I take it as the deemed allotment date for the purposes of interest payment.

Hi Ravi,

Deemed date of allotment is yet to be announced by IREDA. Once it gets announced, I’ll update it here.

Thank you

You are welcome!

Deemed date is 13/03/2014.

Thanks IronBox !!

IREDA tax-free bonds got listed on the BSE & NSE today, March 19th.

Here are the BSE & NSE codes for the same:

8.41% 10-year bonds – BSE Code – 961837, NSE Code – N4

8.80% 15-year bonds – BSE Code – 961839, NSE Code – N5

8.80% 20-year bonds – BSE Code – 961841, NSE Code – N6

Deemed date of allotment has been fixed as March 13, 2014. Interest will be paid on March 13th every year.

What will be the annual interest paymnet date for IREDA bonds.

March 13th every year. It is mentioned in my comment above.

What is the risk of not disclosing exempt income from tax free bonds in IT return?

No idea about the consequences/penalty, if any.

Hi Shiv, do you have an idea when is ITEDA coming out with tax free bonds for fy 2015-16?

Hi Rashmi,

I think you mean the current financial year i.e. FY 2014-15 and not FY 2015-16. This financial year, no company is allowed to issue tax-free bonds. So, IREDA will not be issuing any tax-free bonds in the current financial year.

NON RECEIVING OF INTREST AGAINST TAX FREE BONDS OF IREDA. MY cerificate no. 1229. Folio no. 001406

Hi Dhanesh, you need to contact the Registrar Karvy Computershare for interest payment – http://mis.karvycomputershare.com/ipo/

Sorry, Link Intime is the Registrar for IREDA bonds – http://www.linkintime.co.in/bonds/Default.aspx